Protecting your money from disaster is NOT complicated:

RULE # 1

Don't act on investment advice from anyone (or any company) who is also wanting to broker the transaction. Avoid commission-based "advice". Beware of even "fee-based" fiduciary advisers.

The greatest threat to your savings is conflict of interest. This is covered in great detail on page one. Advice is not free. You must pay for advice. If you go to a "free" adviser (who doesn't directly charge you anything for their advice) this will turn out to be the most expensive "free advice" you'll ever get! If you need personalized financial advice, such as help in selecting investments, then only seek out a fee-only fiduciary adviser on a one-time, one-task or hourly basis. Once completed, process the transactions on your own through a deep discount brokerage. A true fiduciary should never act in the capacity of a product-selling broker. Don't let them process any paperwork regarding investments and don't let them have their name listed on your investment statements as your "broker" (or "agent", "rep", etc). Doing so may entitle them to commissions.

Don't be confused by fee-BASED fiduciary advisers. We call these the "loophole advisors". We come across "fee-based" fiduciary advisers who swear up and down that they make recommendations in the best interests of their clients, but these sneaky clowns still aggressively sell annuities to their clients! This is why an advisor must be fee-ONLY. Use NAPFA.org to find one if you need financial help.

To protect yourself: 1) Make sure you have a written agreement with them which states that they are acting in the capacity of a fiduciary, fee-only adviser. They must provide you with copies of both parts of a "Form ADV", and provide you with a written disclosure of exactly how he will / may be compensated for his services and list any potential conflicts of interest. 2) Finally, make sure that you do your own trading through a discount brokerage (TD AmeriTrade, Schwab or Fidelity) which are merely custodians of your money and investments. Do not allow your adviser's name to be listed on your brokerage statements (as "agent", "broker", etc). If your deep discount brokerage firm can't execute trading for a particular security then consider that recommendation unsafe or a conflict of interest. Don't invest in it! 3) Also avoid "asset managers" who charge you on an ongoing basis, year after year. You want a one-time consultation to come up with a "game plan" and to build a simple portfolio of index funds.

This rule also applies to everyone else under the sun including "venture capitalists" or that good friend who needs investors to invest in a private business or other private equity. Obviously you should not take investment advice from company A when company A is also pitching you the investment (by cold phone calls, on TV or radio infomercials, in print advertisements, emails, via a friend's referral, etc). These people don't spend their time pushing investments without conflict of interest.

TRAP: A person who appears to have no interest in pitching you an investment usually has their own hidden agenda. Why else would they volunteer their time pitching it? For example: They may be pitching the investment for a friend who will pay them a nice "under the table" commission if they get you to invest in it. If it's a scarcely traded penny stock they may be looking for a way to cash out of their own position in the stock. Scarcely traded micro cap and penny stock prices can be easily manipulated by just a few investors or advertising campaigns.

RULE #2

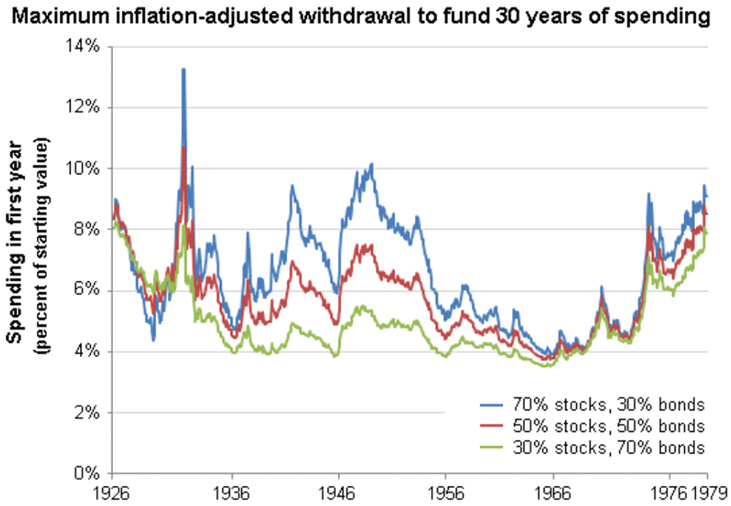

Learn about the 4% rule (AKA the "safe withdrawal rate")

Spending as much as 1% less per year in retirement can have huge implications on whether your nest egg will last or not. For example, a retiree with $100,000 (invested in the S&P 500 index) who spent 5% per year (increasing each year with inflation) starting in 1972 ran out of money after 24 years. Had the same retiree lowered their spending rate to 4%, their portfolio had grown to over $500,000 after 24 years!

How many times have we read about wealthy pro athletes running out of money because they spent like drunken sailors? But sometimes it's everyday people who aren't as careless, but one day still get caught by surprise. Few people really take the time question the sustainability of their spending habits going out 20, 30, 40 or 50 years. How do you know if you have enough money to retire on? How do you know how much of your retirement money you can safely spend without one day running out of money? A good rule of thumb used by financial planners is the 4% rule when looking at a 30 year time horizon (30 years of life expectancy). For example if you have saved up a million dollars then you should be able to safely spend $40,000 per year. As your million dollars increases in value, the actual dollar amount that you can take out increases. This 4% rate allows for cost-of-living increases every year and accounts for expected investment returns, all based on back-tested performance history of the bond and stock markets going all the way back to even before the great depression. The "4% rule" is actually a conservative "guideline" -- not an iron clad "rule". You may be able to spend more or you might need to spend less. Even with a super low-risk 30% stocks /70% bonds mix, there have been starting points from which you could have taken out as much as 8% without running out of money, as illustrated in this chart.

The 4% rule should be re evaluated over time. Just because your principal investment value may start to falter isn't the end of the world and doesn't mean you can't adjust your withdrawals lower. Interestingly the worst year to retire was not right before the 1929 stock market crash but rather 1969, right before there was double digit inflation in the 70's. When you have a 40 year time horizon or greater, the experts recommend spending no more than 3.3% per year. When you have only a 20 year time horizon, studies indicate that the safe withdrawal rate can be increased to between 5.1% and 5.5%, depending on which study you choose to believe.

RULE # 3

Don't invest more than 5% of your savings into any one investment or "fund"

With the exception of cash and index funds, don't put more than 5% of your savings into any one investment or "fund". This is as simple as the old phrase "don't put too many eggs in one basket". Shockingly investors break this golden rule constantly and then we hear about them in the news or on MSNBC's "American Greed". Had some of the victims of Bernie Madoff's Ponzi scheme followed this simple rule, they wouldn't have lost their entire life savings. And even if the investment is not a Ponzi scheme, it's just plain risky to place large bets on one investment. Lower your limit to just 1% or 2% and you are taking even less risk.

Note that it's OK to hold up to 10% in gold (as recommended by Jim Cramer). Also this rule does not apply to personal possessions such as the home you live in, which you generally don't count as "savings".

Index funds are inherently diversified. With index funds you can divide the number of holdings to calculate how diversified you are. For example an S&P 500 index fund like VOO or SPY represents 500 stocks. You are fully diversified when you own a broad market index fund. It may seem like paranoia, but you may want to consider diversifying amongst companies who offer index funds. For example you can diversify amongst SPDR, PIMCO, iShares, etc.

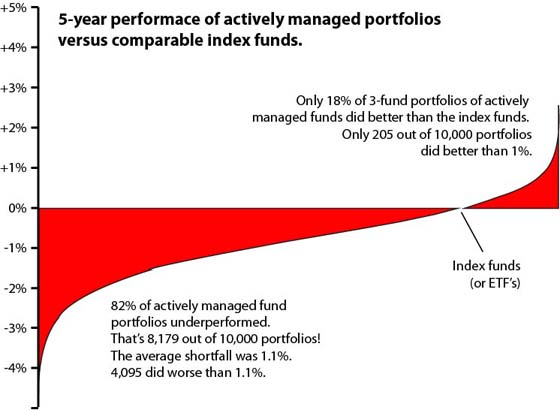

Publicly traded mutual funds are also diversified into many different holdings, however we don't recommend actively managed mutual funds because they generally under perform index funds.

{kind=link}

TRAP: Just because a "fund" is diversified into many different stocks, bonds, etc does not necessarily mean that you are diversified. As previously mentioned, Bernie Madoff's Ponzi private equity fund was supposed to be a "hedge fund" full of many different investments. Unfortunately the entire fund was an elaborate scam. Some funds such as annuities (which should be avoided anyway) invest in a diversification of stocks and bonds, but your entire investment may hinge on the solvency of just one single insurance company that writes the annuity contracts, then dependent upon your state guarantee fund, which could become depleted in the event of systemic failure of multiple insurance companies. Executive Life Insurance Company was supposedly "safe and secure" but it became insolvent. Beware that there have been privately offered certificates of deposit that have turned out to be Ponzi schemes, as was the case with Stanford Financial Group.

RULE #4

Diversify! Avoid over-allocation.

This rule is slightly different than rule #2. You might do the right thing by allocating your money into a variety of investments that don't exceed 5%, but still somehow manage to put your money dangerously at risk. For example one might make the mistake of investing too heavily into to one city, too heavily in one sector (example: the semiconductor sector), too heavily in high risk investments, too heavily weighted in anticipation of a market crash, etc. Or one might make the mistake of positioning themselves in nothing but or too much in stocks, or real estate, or gold, or cash, nothing but bonds, small cap stocks, foreign stocks, etc. In 2008 we found out just how risky investing in real estate can be. In 2020 we found out that investing in student housing was no safe haven. Rich Uncles BRIX REIT lost 93.6% as a result of coronavirus. Some people have a false belief that real estate is "very safe" but don't understand the compounded risk that they are taking by purchasing property with borrowed money. By 2009, once mega-wealthy NBA athletes declared bankruptcy. Some retirees who were over-allocated into stocks (and not enough bonds) had to go back to work. The experts say wealth is built the slow gradual way, one year at a time -- Not by taking excessive risks.

Bond / stock diversification was critical for retirees from 2000 to 2009? When stocks fall, money runs to the safety of bonds. The two balance each other out. Diversification smooths out the volatility that will otherwise kill a portfolio.

For help on how much risk to take or where to invest take a look at Vanguard's portfolio creation tool or EasyAllocator.org. Of course hiring a fee-only fiduciary adviser for a one-time consultation is also recommended.

RULE #5

Avoid investing through private or independent financial services firms or holding companies.

Step one in preventing the possibility of your money getting into the wrong hands is to steer clear of private financial services companies. Are there honest private investing firms? Of course there are. But the average investor doesn't know how to tell the good from the bad. That's why this one simple line of defense could literally save you from financial ruin.

Stanford Financial Group was a privately held financial services company with 50 offices in several countries. Stanford Financial Group even had it's own bank. Some clients invested their entire life savings into Stanford Financial Group issued certificates of deposit. Unfortunately the operation was a giant Ponzi scheme! This underscores the importance of entrusting your money with a bellwether financial services company such as Charles Schwab or AmeriTrade.

This is not to say that you should avoid independent advisory companies and long as you're going to them for pure advice, and you're not actually handing your money over to them. A pure advisory company will recommend that you entrust your money with and invest through your discount brokerage.

RULE #6

Avoid investing in private equity! Only invest in publicly traded investments that are 1) sold on a stock exchange, 2) traded through bellwether discount brokerage firms and 3) can be researched on everyday financial sites like Yahoo Finance.

Publicly traded stocks, bonds, and index funds are the safest investments because they are monitored and regulated to death at many levels. You may have been spooked by stories about corruption at Enron, but these are rare instances. Even if you invest in just one index fund such as SPY, that one bad apple will hardly effect the entire fund. Some index funds are comprised of hundreds of securities.

Investing in private equity is the fastest way to lose 100% of your investment. How many times have we heard stories of pro athletes investing in private businesses and losing it all? It seems glamorous, sexy, and fun but it is anything but. Investors are usually told that private investment opportunities have "enormous potential" but in reality these investments carry huge risk, often fraud is involved, and there is a very high failure rate. Some studies claim that 4 out of 5 businesses fail within the first 2 years. Private equity is so risky that, if you are tempted, you really shouldn't put more than 5% of your money into such investments. Also you should be OK with losing 100% of your investment.

Another line of defense is to avoid any investment that involves signing a contract. Placing an order to invest in an index fund, stock, or bond is as simple as making a few clicks of your mouse through TD AmeriTrade or Charles Schwab.

If you can't research a fund, bond, company stock, commodity or other investment on everyday financial sites then how can you know details about an investment, inspect it's balance sheet, know what is the fair "market price" of the investment, etc??? Just because a stock is listed on Yahoo Finance does not in and of itself mean that it is safe. As previously mentioned, avoid scarcely traded micro cap and penny stocks, for which prices can be fraudulently manipulated.

RULE #7

Avoid illiquid investments. Avoid expensive investments.

There is no need to lock your money in prison. Avoid investments that require you to lock your money away for years and years. That means avoid any investment that has either a "front end load" fee or "entry fee", or "back end load" fee, "contingent deferred sales charge", "early withdrawal penalty", "early exit fee", "redemption fee", "surrender fee" or any other name for a large fee that penalizes you for not remaining in the investment for "X" amount of years. The exceptions are certificates of deposit and individual bonds and US treasuries, although there are liquid index funds that seek to replicate treasuries, bonds, etc. Anyone who tells you that you need to invest in illiquid investments is trying to sell you a high commission based product, and is almost certainly a commission-based "adviser" who doesn't directly charge you any fee. They're either an insurance salesman, bank employee, broker, or broker going by a deceptive title like "financial planner", "investment strategist", etc. These people indirectly make lots of money when you bite on the products that they sell. Then one way or another you pay the price.

Avoid investments that charge a large initial fee for the supposed "privilege" to invest in it. For example with Class A mutual funds, you can freely cash out of the fund at any time without penalty, but you initially pay about a 5.25% front-end load fee or they get you with high annual fees. Even actively managed mutual funds that have no front or back end load fees simply compensate by raising their annual fees (known as "expense ratio"). With “actively managed” mutual funds, one way or another you are going to get fee'd to death. Beware that a deceptive broker may not even disclose the existence of a front end load fee. You might not even notice it because the load fee merely gets subtracted from the initial value of your shares. So if you bought into a mutual fund when it was priced at $25 per share, your entry price would be $23.75. By the time you look at your first statement you might not even notice it because you just assumed that the share price went down with the market.

Conventioinal wisdom says that an investment that requires you to tie up your money for many years, must pay better returns. This may be true of a bank CD versus simply keeping money in a checking account, but not for other financial products. In fact, the opposite is true. For example, when you examine annuities, cash value life insurance products and mutual funds, a sales agent is paid a large up-front commission, the company selling the financial product charges high fees (and/or reduces payout) over time, and in order to insure that they will recoup the agent's commission, they impose surrender penalties.

With bond and stock index funds, you can have the best of both words: 100% liquid (sell at any time for any reason and without penalty) and they are super low cost.

RULE #8

Don't "Chase Yield". The higher the yield, the greater the risk of loss of principal, broken promises, etc. Never confuse interest payment rate with return on investment.

"Chasing yield" is a term used to describe what investors do when they are fed up with the low yields paid by normal investments like utility stocks, consumer staples stocks, US treasuries, certificates of deposit, and they also fear most stock market based investments because they perceive them to be too volatile and risky. Often investors say that what they want in an investment is both "growth" and "safety". Unfortunately these two words are opposites. One is aggressive and volatile, with potential for wild price swings up or down, and the other is conservative and holds up well when the markets crash but misses the train when the market takes off. You cannot have both in one single investment. Don't let any investment adviser try to tell you that he has an investment that is both!!! Many investors fall victim to brokers who sell high commission investments which they falsely characterize as both high yielding and "safe", such as non-traded REITs, limited partnerships, promissory notes, life settlement investments and other oddball investments. They may pay high yields of as much as 10 to 14% but are much much riskier than "advertised". These investments also unnecessarily lock your money in prison for many years. In essence these investments are just too good to be true and sometimes investors loose a lot of money because they took on more risk than they were told by their "adviser".

Annuities and other oddball investments are also often sold under the lure of high annual interest rate payments that are ambiguously referred to as "return". Unfortunately in the end, annuitants never wind up getting that advertised "return" rate as an actual ROI (Return on Investment). In the case of index annuities, "accumulation value" is not the actual cash surrender value or death benefit value that will tell us what the true ROI will be. Insurance companies have clever ways to chip away at the surrender value / death benefit value of your annuity so that your actual return on investment will be much, much lower. In the case of oddball investments like non-traded REIT's, all too often the actual return on investment is never anywhere close to the annual interest payment rate or "accumulation value". Most or all of the interest payments simply represent a return of their original investment money.

Example of how a very high annual interest rate is not what it seems if 100% of your original investment is not returned:

Original investment: $100,000

Annual payment rate: 10% (or $10,000 per year)

Amount of principal returned: Only $70,000

Total of all money received after 10 years: $170,000

Actual ROI (return on investment): Only 5.4% -- Not 10%!!!!!

For a better understanding of what return on investment is you can use this site to calculate ROI.

Examples of what are "high yielding" but not excessively risky include these index funds: XLP (2.56%), SPLV (2.07%), IDU (3.78%). Any investment that pays a higher yield in today's rate environment is either false (as in the case of annuities) or is simply riskier. Despite talk of a "bond bubble" bond funds such as AGG (the total bond market) will never be as risky as stocks on even their worst day.

Keep in mind that there are even publicly traded investments such as junk bonds that pay upwards of 20% yields. As you might imagine these investments carry great risk of broken promises.

RULE #9

Never bear too much or too little risk

This is one of the most basic principals of investing according to John Bogle. You want a balance of stocks and bonds. When you're younger you generally want to have a higher percentage invested in stocks, because if you are also generating income by working, a stock market crash will not leave you devastated. As you approach retirement you generally want to be more conservative. A senior citizen who can ill afford a stock market crash set-back will generally want to be more invested in bond funds (bond index funds). Don't know how much to invest in stocks versus bonds? Check out Blackrock's core portfolio builder. It asks you a few questions then spits out a simple, sensible portfolio that can be replicated with low cost index funds. Also try Ric Edelman's portfolio selection tool. This tool is very helpful in determining what allocation fits your particular appetite for risk, although you do not have to invest in so many flavors of index funds (mid-cap value, mid-cap growth, small-cap growth, small-cap value, etc.). Why not just buy the S & P 500 index to represent your entire stock group? This is what Warren Buffet recommends for the average investor. Want more risk than the S & P 500 index? Throw in a blended mid-cap (VO) and / or a small-cap index fund (VB) and / or a NASDAQ index fund (QQQ). And finally check out Vanguard's nest egg calculator.

The experts will tell you that cash alone is not an "investment" and therefore most people will not want to sit on the sidelines with a large percentage of cash. According to Stanford University's Hoover Institution, during the 20th century, inflation has averaged about 3% per year. So if you're too afraid to take some risk (by investing in stock and bond index funds) eventually inflation will take a significant chunk out of your money.

RULE #10

Never allow anyone to have access to or have control of your money. Invest through a bellwether financial services company.

If you hire an adviser, be sure to go to them for pure advice, then leave and invest on your own through a bellwether company. Do all of your trading through a deep discount brokerage firm like AmeriTrade or through a "light advice" company like Charles Schwab or TD AmeriTrade. Don't entrust your money with or invest through smaller brokerages or financial services companies that might themselves be Ponzi schemes or they might be selling investments that are Ponzi schemes.

Never give anyone the power to execute trades. If there's something that can't be invested in without your "adviser" processing or helping process the transaction then don't touch it! It's probably a commission based product that pays your "adviser" a nice commission. At worst it could be a Ponzi scheme. Several NFL players allowed a financial adviser to place money in unauthorized investments and they wound up losing more than 40 million dollars.

As an extra line of defense, don't allow Mr. Advisor's name to be listed on any investment statement. In doing so this may entitle them to commissions.

The only checks you write should be payable to a big name deep discount brokerage. Never write checks out to the investment guru down the street or to independent advisory firms.

RULE #11

Behavioral finance: Don't try to time the market. Instead just buy, hold and rebalance.

Investors are all too often their own worst enemies when they attempt to time the market, but only wind up essentially buying high and selling low, then repeating the same behavior. This article details how from December 2003 until 2013 the average fund investor only gained an annualized 4.8% while the average fund gain 7.3%.

Take it from economist Burton G. Malkiel that "No one can consistently time the market, and you are more likely to get it wrong than right." This is because the market generally goes up and timing the market requires picking not just a good exit point but also a good re-entry point. Will the next crash happen next month, next year or 4 years from now? And will it be a crash of 10%? 20%? 30% or more and how long will the decline play out for? The odds are working against you. You are more likely to just miss out of market gains by being out of the market. Also some of the biggest market gains have occurred in one trading day or just a few trading days.

Do you cash out of your investments when there's something to worry about? There's always something to worry about! Just ignore doom and gloom headlines.

Making subtle long-term portfolio allocation adjustments is not the same as market timing. Percentage rebalancing helps to mitigate volatility.

RULE #12

Don't buy individual stocks

First of all, trading individual stocks is more expensive. You pile on more trading costs. It's also riskier. Longboard Asset Management examined the returns of 3,000 stocks from 1983 to 2007. 39% of these stocks were unprofitable despite the fact that this period included the great bull market run of the 80's and 90's. Meanwhile the S&P 500 price return index returned 829%. This tells you that there's a real chance that by owning just a few stocks you might lose money or just under perform the S&P 500 index. Of course you could mitigate that risk by buying more stocks, but then you're increasing trading costs, and at some point you might as well just own one single S&P 500 index fund.

Trading individual stocks is antiquated. Due to the rapid dissemination of information, nobody has any advantage over anyone else when it comes to attempting to beat the indexes by trading individual stocks. In study after study, year after year, it has been shown that the vast majority of experts cannot beat their benchmark indexes. Therefore paying someone to attempt to time the market is a waste of money, whether he's the stock picking guru down the street or a Wall Street mutual fund manager.

RULE #13

Understand what an advisor does and does not do

The purpose of hiring an advisor is:

1) Implement a spending strategy. This generally means learning about and adhering to the 4% rule or whichever rule applies to you so that you don't run out of money before you die.

2) Apply an asset allocation strategy. That generally means deciding on a bond/stock allocation ratio that fits your age, retirement goals and appetite for risk.

3) Recommend low cost index funds. Keep in mind that there is nothing wrong with owning as few as 2 or 3 index funds (discussed in rule #12)

These tasks can be completed on a one-time, one-fee or hourly basis. Always be sure to hire a fee-only fiduciary advisor. Do not hire an asset manager on an ongoing basis if all you need is help with 1 and 2 and possibly 3.

Beyond this, the rest is optional and more costly because you must pay the advisor on an ongoing basis, year after year:

4) Act as a behavioral coach by stopping you from making stupid decisions with your money, such as panicking by selling low. Anyone with discipline can do this. If you are panicking when stocks fall then you weren't honest with yourself when you decided on an asset allocation strategy. Also read this article again.

5) Maintain your bond/stock allocation ratio by percentage rebalancing. Anyone can do this.

As always, be sure to hire a fee-only fiduciary advisor if you need as asset manager. Never work with anyone else.

Avoid any advisor who claims that he can pick winning stocks, winning funds or time the market. Advisors are always looking for reasons to make you think that you must continually pay them year after year after year. Many advisors are very knowledgeable about the financial markets. But all of the knowledge in the world can't help you time the market.

RULE #14

Understand that the actual investing part is simple

There is nothing wrong with owning a cookie cutter portfolio of as few as just 2 or 3 index funds to represent your entire portfolio. Think about this -- If you paid an advisor to come up with a personalized portfolio and he just recommended a total stock market index fund and a total bond market index fund and perhaps an international stock market index fund, you might not feel any need to return for any follow up (paid) advice. Perhaps you wouldn't even hire him in the first place because a friend told you how easy investing is. And so advisors always feel compelled to make investing seem complicated. They tell you that you need a large cap growth fund, a large cap value fund, a mid cap growth fund, a mid cap value fund, a small cap growth fund, a small cap value fund, A REIT fund, a natural resources fund, a short duration corporate bond fund, a medium duration corporate bond fund, a long duration corporate bond fund, a short duration government bond fund, a medium duration government bond fund, a long duration government bond fund, etc, etc. Now you feel like you're in over your head. But it doesn't have to be so complicated.

RULE #15

Things to do before you invest

1) Pay off credit card debt. Over the long term there's no way your investments are going to keep pace with that high interest rate that you're paying. 2) Get health insurance. Nothing can wipe out your wealth faster than a few days spent in the hospital. Insurance is something you just must pay for but just hope that you never have to use it. 3) If being out of work for an extended period of time would wipe you out then get disability insurance too. 4) Consumer advocates like Dave Ramsey recommend long-term care insurance for most people starting at about age 60. Dave says that the odds of needing long-term care before age 60 are something like only 1 in 300. However the rising costs of long-term care insurance is something to consider. 5) If you have a significant amount of money to sue for then seriously consider getting an umbrella policy with your homeowner's insurance to help protect yourself from such things as false arrest, libel, slander, invasion of privacy. A million dollar umbrella only costs about $235 per year.

RULE #16

Don't buy into stock market fear.

Study historical returns of stocks and bonds together.

If you are sufficiently diversified into bonds then it doesn't matter if the stock market may happen to be over valued. Yet fear of the stock market is what salesmen (of annuities, services, books, oddball investments, etc) use to get you to fall for their sales pitch. The easiest way to sell something to someone is to scare them. Selling fear was made easier after the stock market slump from May 2000 to March 2009. Investors who were ignorant of diversification (into bonds) lost a fortune from 2000 to 2009 because they were heavily invested in stocks. They then became easy prey for insurance product salesmen and other non-fiduciary hucksters selling oddball investment products. What these hucksters never explain to their victims (clients) is that it wasn't the stock market's fault that they lost their shirts; It was their fault for simply failing to diversify.

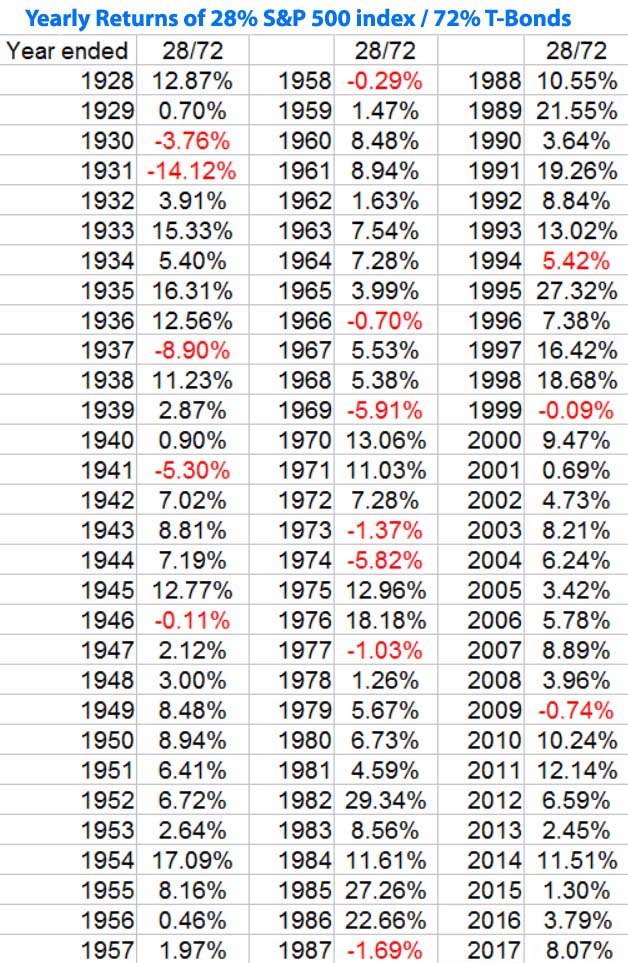

Every conservative investor who is about to be sold an insurance product (annuity, whole life, universal life, variable life, etc) , non-traded REIT or other inferior oddball investment product should study the historical returns of low-risk portfolios, such as 25% S&P 500 stocks and 75% ten-year treasuries (below left) or a portfolio of 33% S&P 500 index / 67% Barclays US Aggregate Bond index portfolio (below right).

RULE #17

Never mix insurance with investing

That means if you need life insurance then only consider term life insurance. Avoid whole life, avoid universal life, avoid variable life, avoid universal variable life and any other insurance product that mixes your investment money with insurance.

Also avoid the other products that insurance agents and other non-fiduciary sharks try to sell you that mix your investment money with an insurance product such as index annuities, fixed annuities, variable annuities and hybrid annuities. While some people claim that immediate annuities (or single premium immediate annuities or SPIA's) are the least offensive of all annuities, these products will provide inferior if not zero returns on investment.

RULE #18

Never attend free seminars. Beware of others who present themselves as "just trying to help" free of charge.

Free seminars are always put on by product pushing salesmen who stand to earn big money if you bite for whatever it is that they are pushing. Ask yourself where that money will come from? From you! And it must come from you either directly or indirectly because money is not created out of thin air. That's why they are volunteering their time and paying to feed you a free dinner and/or to rent out a conference room at a nice hotel. The most commonly pushed investment products include annuities, non-traded REITS, cash value life insurance, and asset management services. All of these products are inferior to low cost index funds. Index funds do not pay commissions to advisers. That's why there are no free seminar gurus pushing index funds.

It doesn't end with seminars. Product pushing salesmen are famous for paying radio air time, then pretending to be part of the regular for-hire on-air talent. The tip off is when they may have a toll free number for you to call during the week. They may also offer to visit with you free of charge to go over your finances with you. Their ultimate goal is the sell you an inferior, expensive financial product for which they will get paid a lavish back-door commission.

RULE #19

Control taxes

If you have a lot of money locked up in expensive investments such as actively managed mutual funds then getting out quickly instead of staggering those sales, might wreak havoc on your finances come tax time. If you somehow have managed to break rule #1 by going to a commission-based adviser (non-fiduciary) then beware of any adviser who suggests that you sell off a lot of your investments in order to shift your money to other investments. In doing so you may be greatly increasing your taxes.

If you own an annuity then doing a 1035 exchange out of your expensive retail annuity (that Mr. Adviser sold you) into a TransAmerica annuity could save you loads of money and continue to compound the savings for years to come. If you are perhaps age 56 or younger, then starting a SEPP (substantially equal periodic payment) program will help you get a head start out of that annuity that is dragging down your returns.

RULE #20

Take the time to learn about managing your money

You hear a lot of people say "I don't have time to learn about managing my money. That's why I need to hire someone to do it for me". Most people need help, but putting all of your trust in someone else can have disastrous results. You must learn to manage your money! Think about how many years or decades it took to earn that money. Then think about putting in a tiny fraction of that time into learning how to manage and invest it. Just reading this web page alone will put you further ahead of the game than 99% of investors.

NEXT ARTICLE: Index funds aka "Exchange Traded Funds" aka "ETF's" aka "passively managed mutual funds"

Disclaimer and Waiver - Nothing on this consumer advocate website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy, hold or sell, or as an endorsement, of any company, security, fund, product or other offering. This website, its owners, affiliates, agents and / or contributors are not financial or investment advisors or broker / dealers and assume no liability whatsoever by your reliance on the information contained herein. The information should not be relied upon for purposes of transacting securities, assets, financial products or other investments. Your use of the information contained herein is at your own risk. The content is provided 'as is' and without warranties, either expressed or implied. This site does not promise or guarantee any income or particular result from your use of the information contained herein. It is your responsibility to evaluate any information, opinion, advice or other content contained. Always hire and consult with a professional regarding the evaluation of any specific information, opinion, or other content.