The Efficient Market Hypothesis

Increased “Market efficiency” has made it very difficult for managers to beat the market

In recent years the market has become very “efficient”. What does that mean? At any given time, stock prices very accurately reflect all available information on a particular stock and the broad market. What does that mean for professional managers and soccer moms alike? Nobody has any advantage over anybody else because with computers and the Internet, information is available instantly and market trades happen in seconds. Nobody should be able to “beat the market” when picking stocks, and nobody should be able to “time the market” for that matter in trying to anticipate broad market movements as a whole. Years ago Wall Street managers had an edge when news was slow to travel. Things have changed with the Internet, and statistical evidence supports this theory. High-frequency trading, while criticized and hotly debated, has actually had a positive side effect in that it has helped make markets more efficient.

In recent years the market has become very “efficient”. What does that mean? At any given time, stock prices very accurately reflect all available information on a particular stock and the broad market. What does that mean for professional managers and soccer moms alike? Nobody has any advantage over anybody else because with computers and the Internet, information is available instantly and market trades happen in seconds. Nobody should be able to “beat the market” when picking stocks, and nobody should be able to “time the market” for that matter in trying to anticipate broad market movements as a whole. Years ago Wall Street managers had an edge when news was slow to travel. Things have changed with the Internet, and statistical evidence supports this theory. High-frequency trading, while criticized and hotly debated, has actually had a positive side effect in that it has helped make markets more efficient.

In theory, market efficiency should apply to not just mutual fund managers, but newsletters and the local asset manager / stock picker down the street who may attempt to time the broad market, favor one stock over another, favor one asset class over another, favor one risk strategy over another, etc.

In late 2012 some investors were talking about moving their money to safety in anticipation of the "fiscal cliff", but everybody already knew that the fiscal cliff was coming. The fiscal cliff was already factored into market prices. Whether the market moved up or down the next day was to be determined by news that had not yet been reported. Nobody knows what will be reported in the next day's news and so nobody can predict where individual stocks, bonds, real estate, gold, or the market as a whole will move -- not mutual fund managers, not asset managers, not soccer moms.

In theory the only way that one can beat an efficient market is by simply taking more risk and hoping for the best. Of course by taking risk you can just as easily under perform the market. So for example, instead of buying an index of 500 stocks you could take more risk by buying just 1 stock and expect to see wilder price swings. Or instead of just buying and holding you might attempt to "time the market" by hopefully buying low and hopefully selling high. In theory beating the market does not involve skill, but rather getting lucky after taking a risky guess.

Do you need a financial adviser to help you initially?

I say that most people do at least need a one time consultation to help in selecting a mix of investments based on such factors as their age, income needs, etc. One of the reasons to hire a fee-only fiduciary adviser is so that they can protect you from making stupid mistakes such as over-allocation, running to the safety of bonds after the market has already collapsed, investing in private equity, etc.

Are there people who do it without any help? Absolutely. Do-it-yourselfers have outperformed most Wall Street professionals by following some incredibly strategies. Warren Buffet has said that by just investing in one broad market index fund like SPY you are likely to outperform most Wall Street pros. Other simple approaches might include a simple combination of two ETF's like SPY and BND, basing how much percentage you invest in each on your age. Many investors do it themselves with the popular and simple Boglehead philosophy of investing. Financial advisers would like you to believe that investing is complicated. It doesn't have to be. You don't have to get fancy to outperform the pros.

Should you hire a full time "asset manager" at a cost of about 1% to 2% per year?

If you hire a financial planner for a one time consultation to help you select investments, they may try to get you to hire them to constantly oversee your investments. But you will need to decide if this is really necessary or not, as their “asset management" fee will shave perhaps 2% (average fee) off of your savings every year. That’s a lot to have to make up for each and every year. Is this really necessary especially when considering that the statistical evidence is clear that unmanaged indexes (ETF’s) have consistently outperformed professionally managed mutual funds and market efficiency works against professional managers? And if you are somehow persuaded to invest in expensive "actively managed" mutual funds, you are effectively paying a manager to manage still more paid managers! In this situation your total annual cost of having all of these managers might be between 5% and 6% per year! Chances are that each year an asset manager will simply ask you if your financial goals, income needs and appetite for risk has changed and then make adjustments accordingly. Or if one fund has significantly outperformed the other he might recommend re-balancing your portfolio. But is this rocket science or can you do it yourself, thus saving 2% per year? That is for you to decide.

Will a full time "asset manager" really get my money to safety ahead of a market collapse?

A lot of investors just assume that an asset manager will anticipate a massive market collapse and move their money to safety before it happens, as it starts to happen, or before it starts to really collapse. But is that realistic? Consider this: 1) Statistical evidence has demonstrated that wall street mutual fund managers as a whole don’t outperform indexes during declining markets. 2) The concept of “market efficiency” says that nobody has any advantage over anyone else, and that the markets are always fairly priced at any given time. How do you predict the future?

Ask yourself, during the 50% plus market decline that lasted from October 2007 through March 2009 how could any asset manager really have 1) predicted the decline and 2) predicted the bottom and 3) at the risk of being wrong and losing angry clients, is it likely that any responsible asset manager would actually recommend that his clients make significant changes to their portfolio soon enough and gotten them back in soon enough to enjoy a net gain that would offset the asset manager fees? Remember that any decision to get out of the market must have a decision to get back in too! Both are perilous decisions that can easily backfire!

The danger of being out of the market

Many experts have concluded that there is more danger of being out of the market, and that timing the market just doesn't work. It is a fact that some of the biggest stock market moves upward have occurred in single trading days! Miss out on these one day gains (because you ran for cover) and it can greatly affect your long term returns!

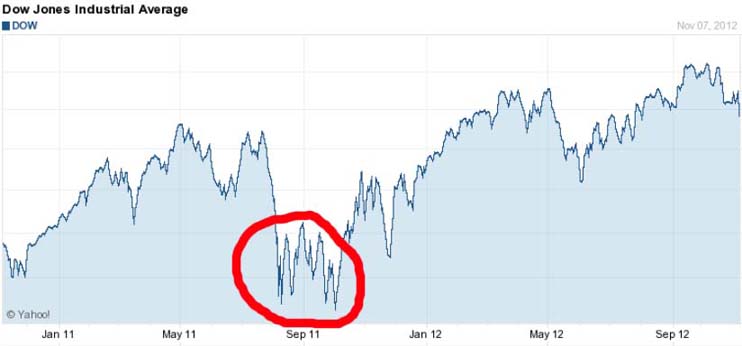

After the market goes down 10% or 20% how do you really know if the "crash" is over and done with? In 2010 when the Dow dropped below 11,000 a pro-active "asset manager" might have feared the worst and recommended that his client get out of the market. This would have been a costly mistake as the DOW has continued on its bull run.

BELOW: A "pro-active" asset manager's nightmare

"Irrational exuberance" speech: An example of a market timer's nightmare

On December 5, 1996 federal reserve chairman Alan Greenspan warned of overly inflated stock prices in his now famous “Irrational exuberance speech”. At that time the Dow Jones Industrial average was at 6,437.10. Anyone who took that as a cue to make dramatic changes by selling off lots of their stock holdings missed out on a continuation of that bull market as the Dow proceeded to go up another 75% in less than 4 years!

On December 5, 1996 federal reserve chairman Alan Greenspan warned of overly inflated stock prices in his now famous “Irrational exuberance speech”. At that time the Dow Jones Industrial average was at 6,437.10. Anyone who took that as a cue to make dramatic changes by selling off lots of their stock holdings missed out on a continuation of that bull market as the Dow proceeded to go up another 75% in less than 4 years!

So again, do you really want an asset manager attempting to “time the market” with your money? I wish I had a nickel for every newsletter or "investment expert" who accurately predicted over valuation but jumped the gun way too soon. All too often the "experts" will cry over-valuation [of an investment or asset class], but then prices will still continue upward for a significant period of time. Eventually prices might correct but not enough to justify getting out of the market so early. Also it is common that experts will still mange to give themselves "credit" for predicting a price drop even though it cost the early birds money because they missed out on continued gains.

What is an active asset manager likely to do?

Asset managers generally just diversify amongst investments based on your appetite for risk. Then they hope for the best while making simple allocation adjustments over time as one group of investments might outperform the other. Anyone can effectively do this on their own with ETF's! More than likely the role of a full time asset manager is only going to be to merely advise the client against urges to make glaringly stupid mistakes such as if a client panicked and wanted to switch a huge percentage of their portfolio from stocks to bonds after the market had already fallen 50%. Back in 2008 - 2009 some investors foolishly did just that. Reacting to news after the fact is a fools game. Reacting to old news is akin to selling low and buying high.

Timing the market is not only dangerous (as described above) but can potentially expose an asset manager to malpractice lawsuits and so pro-active asset managers may actually refuse to recommend making dramatic changes to a portfolio. This only makes it less likely that an asset manager is going to make up for that annual 2% fee that he is charging you.

"I'm happy with my asset manager"

The question is does your asset manager really have the ‘hot hand’ for picking investments, or did he just take risks and get lucky?

Just how much risk did your investment adviser expose you to in order to get the return that you got?

Let’s say that you’re 60 years old and so you want very moderate risk. You might go with the typical 50% of your savings in fixed income assets (bond and cash investments) and the other 50% in stocks. But let’s say your “investment adviser” convinces you to invest $50,000 in a limited partnership that is supposed to pay 6% interest per year, and split the remaining $50,000 into Apple, Clorox and Con Edison stock. You might be happy if your stocks went up 15% in one year while the Dow only went up 10% during that same period. And you might be thrilled that you received a 6% return on that risky limited partnership rather than the paltry return of less than 2% that you would have received from a US Treasury bond. But what really happened is that a broker simply exposed you to more risk and you got lucky. It could just as easily gone a much different direction. Don't give your adviser credit for simply exposing you to more risk.

Another question to ask is have you made an apples to apples evaluation? What kind of returns are you getting relative to comparable benchmark averages?

If an “investment adviser” sold you a small-cap growth mutual fund, don’t compare its performance with the Dow Industrial Average or the Wilshire 5,000 index. You should do an apples to apples comparison of its performance (factoring in fees) and against the small-cap growth index or comparable ETF’s like VBK. Do the same apples to apples comparison for each individual fund. Every mutual fund should have a "benchmark" index fund from which to compare it to. If your “investment adviser” is acting as a fiduciary and charging you an annual fee to manage your money then factor that in as well to see if you are really beating the market.

You can also compare the total return versus just one benchmark such as SPY (S&P 500 index ETF).

You might also compare all stock funds versus SPY and your total bond investments versus an index fund like BND (total bond market).

MY CONCLUSION: Remember that the S&P Index has outperformed the vast majority of active mutual fund managers. So by banking on active managers to beat the market you are going against the grain by "betting against the house" so to speak. The efficient market hypothesis says that all you have to do is just buy and hold plain old index funds - also known as "Exchange Traded Funds" (ETF's) or "Passively Managed Funds".

NEXT ARTICLE: Film investing

Disclaimer and Waiver - Nothing on this consumer advocate website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy, hold or sell, or as an endorsement, of any company, security, fund, product or other offering. This website, its owners, affiliates, agents and / or contributors are not financial or investment advisors or broker / dealers and assume no liability whatsoever by your reliance on the information contained herein. The information should not be relied upon for purposes of transacting securities, assets, financial products or other investments. Your use of the information contained herein is at your own risk. The content is provided 'as is' and without warranties, either expressed or implied. This site does not promise or guarantee any income or particular result from your use of the information contained herein. It is your responsibility to evaluate any information, opinion, advice or other content contained. Always hire and consult with a professional regarding the evaluation of any specific information, opinion, or other content.