FACT: Three out of four U.S. investors mistakenly think that financial advisors at brokerage firms are required to put client's interests first. Source

According to the White House Council of Economic Advisers, conflicts of interest shaves off on average 1 percent per year from retirement savings.

"Bad advice that results from conflicts of interest costs middle-class and working families about $17 billion every year" -- Barack Obama

"I have never seen a time when there were more sharks than there are now."

-- Bob Brinker, money talk radio host of 30 years

The biggest threat to your retirement savings is actually the very professional you go to for money advice. When advisors earn back-door commissions (that you probably don't even know about) this conflict of interest costs you dearly. Even though Mr. Advisor might not have charged you anything, his advice became the most expensive "free advice" you could ever get! That so-called trustworthy professional was nothing more than a self-serving salesman trying to leech off of your savings by selling you expensive, inferior-performing, long-term commitment products like annuities, cash value life insurance, non-traded REITS, actively managed mutual funds, etc. Even as a "fee-based" asset manager, whereby Mr. Advisor openly charges you quarter after quarter, year after year, his advice becomes tainted and a major and unnecessary drain on your pocket book.

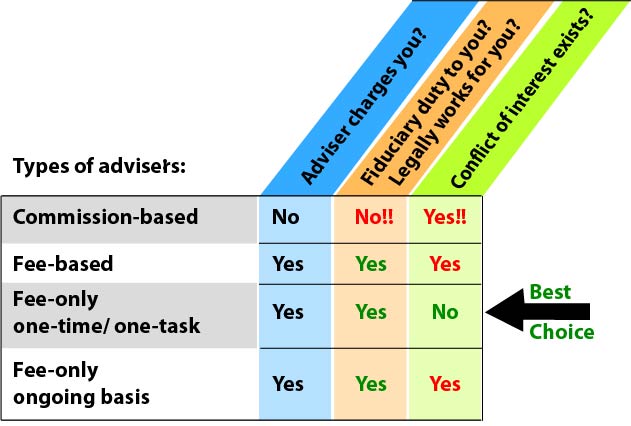

Investing is easy. But if you still need to work with an advisor, then two of the most important terms that you must learn about are "fiduciary" and "fee-only" (no back-door commissions for Mr. Advisor). Do you even know if you are working with a fee-only fiduciary advisor? We constantly see commercials for large brokerage firms and others who imply that they are on your side. But are they really? Shockingly about 85% of investment professionals in the US are not fiduciaries, and most investors don't even know what a fiduciary is. Of the remaining 15% that are fiduciaries, most are merely fee-based salesmen who find creative ways to serve their own best interests at your expense, such as by aggressively pushing high-commission index annuities, which are inferior financial products.

A fiduciary advisor has a legal duty to select investments for you that are in your best interests, whereas a non-fiduciary is legally allowed to select inferior, more expensive investments for you  based on how much back-door commission money he stands to earn from the transaction, which comes indirectly at your expense! In other words, with non-fiduciary advisors, conflict of interest is perfectly legal! In fact if they want to stay in business they must sell you those expensive, inferior products that pay themselves under the table commissions. Ask yourself why else would they be meeting with you to go over your finances for free? They call themselves "advisors" but in reality they are nothing more than SALESMEN attempting to convince you to buy expensive financial products so that they can get paid back-door commissions for each transaction. Legally these "advisors" work in the best interests of themselves (or their company). By default you can expect to be sold expensive actively managed mutual funds with either high expense ratios (fund management fees) or front end loads, or other inferior, illiquid, "alternative", riskier and vastly more expensive investments. This conflict of interest is perfectly evident when you compare "passively managed" mutual funds with "actively managed" mutual funds or when you compare annuities to a diversified mix of stock and bond index funds. You think that you're getting a bargain because your advisor doesn't directly charge you any fees, or perhaps because he sold you a "no-load" investment product that outwardly appears to be free of fees, when in reality you are being indirectly taken to the cleaners. Most investors are completely unaware that they are being fleeced. You may even become a victim of excess trading (or churning as covered near the bottom of this page).

based on how much back-door commission money he stands to earn from the transaction, which comes indirectly at your expense! In other words, with non-fiduciary advisors, conflict of interest is perfectly legal! In fact if they want to stay in business they must sell you those expensive, inferior products that pay themselves under the table commissions. Ask yourself why else would they be meeting with you to go over your finances for free? They call themselves "advisors" but in reality they are nothing more than SALESMEN attempting to convince you to buy expensive financial products so that they can get paid back-door commissions for each transaction. Legally these "advisors" work in the best interests of themselves (or their company). By default you can expect to be sold expensive actively managed mutual funds with either high expense ratios (fund management fees) or front end loads, or other inferior, illiquid, "alternative", riskier and vastly more expensive investments. This conflict of interest is perfectly evident when you compare "passively managed" mutual funds with "actively managed" mutual funds or when you compare annuities to a diversified mix of stock and bond index funds. You think that you're getting a bargain because your advisor doesn't directly charge you any fees, or perhaps because he sold you a "no-load" investment product that outwardly appears to be free of fees, when in reality you are being indirectly taken to the cleaners. Most investors are completely unaware that they are being fleeced. You may even become a victim of excess trading (or churning as covered near the bottom of this page).

Understand the difference between commissions and fees

Commissions = Money paid behind the scenes ("back-door") to a broker / advisor (agent or other salesman) by the company that offers securities or financial products (such as annuities and mutual funds) when the advisor manages to convince the client to invest in the security. This commission is not created out of thin air. It puts a drag on the investment so that the investor actually indirectly pays the high commission.

Fees (salary) = Compensation paid from client to advisor as legal consideration for services provided.

Why do advisors push inferior, expensive, long-term products rather than low cost, liquid, superior performing index funds? Look no further than the lavish back-door commissions...

Fixed Index Annuities: The top 10 best selling index annuities averaged 11% commissions. Some as high as 20% have been reported. Plus a possible trailer commission of typically around 1/4% per year for as long as you hold the annuity or have the agent's name listed on your statements. The commission amount is likened to the surrender period length.

Variable Annuities: About 7% - 10% up front, plus a possible trailer commission of typically around 1/4% per year for as long as you hold the annuity or have the agent's name listed on your statements. The commission is likened to the surrender period.

Investment-grade (cash value) insurance policies like whole life, variable life, universal life, indexed universal life, etc: Generally 100% of the first year’s premiums then 6% of the premiums for every year thereafter. By comparison, term life insurance pays agents only 50% of the first year’s premiums, then only 4% of the premiums thereafter.

Life Settlement Investments: About 4% - 8%, but as much as 15%.

Non-Traded REITS: Usually over 10%

Limited Partnerships: Anywhere from 1% – 10%, followed by a 1 – 2% annual trailer commission.

Immediate Annuities: 3% - 4%

Actively managed mutual funds: 2% - 4%

Individual municipal bonds: Average 2%

Individual corporate bonds: Average 1.25%

Index funds: NO commission! Now you know why commission-based "advisors" never recommend index funds, even though index funds are tax efficient, super low cost and superior performing.

Sources: Kiplinger , WikiFool, ProbateLawyerBlog , TheREITAdviser , HighPassAsset , CrimesOfPersuasion , Quatloos , Forbes Magazine

How much do fee-ONLY fiduciary advisors earn in commissions?

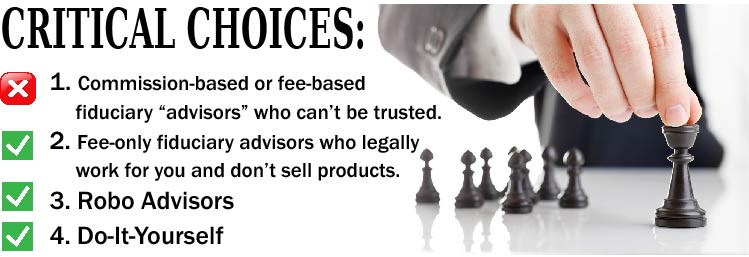

Nothing! Legally a fee-only fiduciary advisor are compensated from you and you only, and this cuts out the worst conflicts of interest. Choose to work with them on an hourly, one-time or one-task basis and then do your own trading through a deep discount brokerage (such as AmeriTrade, E Trade or Scottrade) to most effectively eliminate conflict of interest. This is easily your lowest cost option. Shop around until you find a reasonably priced advisor for the task you require.

Fee-only on an hourly basis is the best and only choice if you need money advice

The best legal line of defense in weeding out conflicts of interest is to seek out a "fee-only" fiduciary advisor (rather than a "fee-based" fiduciary advisor) because "fee-only" means that legally they cannot earn compensation from any source other than you. Fee-only advisors legally may not earn compensation from transactions, which means that at least legally there is no opportunity for conflict of interest resulting in you being sold inferior products like annuities, actively managed mutual funds and other oddball investment products. Be sure to hire them on an hourly basis -- not as an ongoing asset manager. Rebalancing index funds does not require ongoing professional help.

CONSUMER ALERT: A big warning about fee-based fiduciary advisors

CLICK HERE to read about why by default, even fee-based fiduciaries should not be trusted.

Beware of dually licensed (or dually registered)

and "hybrid" advisors!

Some advisors are dually licensed as either a fiduciary or non-fiduciary. Unscrupulous advisors may say one thing then do another. They trick you into believing that they are serving you in the capacity of a fiduciary when in fact they are nothing more than commission-hungry salesmen.

And a "hybrid RIA" is registered as both an RIA and a broker/dealer. Not surprisingly these types of advisors all too often cannot resist the urge to recommend high-commission products such as those dreaded annuities.

Beware of supposedly unbiased gurus who direct you to someone else who in turn sells you high commission products like annuities

In order to create the appearance of being unbiased, some product pushing salesmen (often annuity salesmen) will simply direct you to a second person or business entity, which in turn makes the high commission sale. Then the first salesman that you spoke to gets to earn his back door commission from the second person who actually executed the sale. One such example is Tony Robbins, who puffs up index annuities, which are highly inferior financial products. Another appears to be Greg Fox who styles himself as being "retired" and "just trying to give back" when in fact he is a licensed insurance agent. On his radio infomercial, which is dressed up as a "radio show", he makes a one-sided, hard sales pitch for index annuities.

A verbal agreement isn't worth the paper it's written on

It is critical that Mr. Advisor memorializes their fiduciary duty to you in writing once per year. They should provide you with both parts of what's called a "Form ADV" with written disclosure of exactly how he will / may be compensated for his services and list any potential conflicts of interest. They should also do so on an annual basis so that they don't lapse into becoming a fee-based fiduciary or non-fiduciary. Do not work with any advisor who does not provide you with all of these critical documents.

Fiduciary laws are only a legal line of defence

A WORD OF CAUTION: Never lose sight of the fact that the fiduciary standard is only a legal line of defense. It's very strong one but some brazen advisors may flat out break the law, risking suspension, being barred from the industry, and even jail time. This firm boasted of having fiduciary registered investment advisors but as it turns out was running a Ponzi scheme. These advisors held themselves out as "fee only" but were pushing commission-based products. This underscores the importance of not just having a written contractual agreement, compensation disclosure documentation, etc but also learning which investment products to avoid, what basic rules to follow and other lines of defense such as doing your own trading and without your advisor's name being listed on your brokerage statements. Nobody has your best interests at heart more than you.

Nothing good is free

If you can't do-it-yourself then the bottom line is that the superior choice is either to go to a fee-only fiduciary advisor working on a one-time or one-task basis or go to a light advice company such as Vanguard, Fidelity or Schwab. Vanguard only charges 0.3% per year. You do NOT want to work with the free guys (commission-based advisors who sell you expensive products). This is the most expensive "free advice" you will ever get! The free guys will cost you much much more over time.

Click here to find a fee-only advisor in your area. Again be sure to first read on this site about how to avoid being taken advantage of.

Some question where is the potential conflict of interest with an on-going fee-only fiduciary "asset manager" who charges you perhaps monthly, quarterly or annually. If the advisor charges you based on the dollar value of your account then if you ask for advice on what to do with money that you are considering investing in things like real estate or metals then a NO recommendation might be due to conflict of interest. Asset managers are also always going to try to convince you that you need them to constantly manage your money (and bill you).

The art of deception begins by flashing titles and certifications

Insurance agents and registered representatives (brokers) know that titles like "insurance salesman" or "securities salesman" do not convey trust, and so they look to flash their certifications or name themselves by some other trustworthy sounding title. This is step one in gaining your trust!

CFP (Certified Financial Planner), IAR (Investment Advisor Representative), CRPC (Chartered Retirement Planning Counselor), CLU (Chartered Life Underwriter), ChFC (Chartered Financial Consultant), RICP (Retirement Income Certified Professional), CEBS (Certified Employee Benefit Specialist), CEA (Certified Estate Advisor) are some of the many certifications that might lead one to believe that an advisor can be trusted to give unbiased investing advice in your best interests. Certifications are fine and dandy but they say nothing about what is most critically important: Whether they are fee-only or not -- Whether they will make recommendations that are best for you, rather than for themselves (back door commissions).

If they don't have some fancy sounding certification then they can just dream up a trustworthy sounding title for themselves like "chief investment officer, "wealth advisor", "senior wealth advisor", "wealth architect", "wealth manager", "retire mentor", "senior financial services executive," "investment advisor representative", "financial advisor", "advisor", "financial planner", "vice president", "investment consultant", "investment strategist", "account executive", "retirement planning expert", "investment advisory services advisor" or any other title of their own choosing that gives the impression that they are trustworthy in recommending investments or strategies that are in your best interests. They have paid a company to become a New York Times "best-selling author". Never make the mistake of using a commission-based advisor for money advice. These guys should be regarded as nothing more than salesmen who are driven to execute transactions that pay back door commissions (indirectly at your expense).

A fancy sounding credential like CFP does not tell you whether an advisor has fee-only fiduciary duty when recommending financial products. In fact the CFP board will not say that all CFP's are fiduciaries. There's lots of CFP's out there who aggressively push inferior products like annuities. That should tell you everything about that advisor's priorities because annuities (other than Vanguard) are commission-based products. For that reason you might just call them "Certified Financial Parasites"! Some but not all CFP's get disciplined. When it comes to selecting investments, by default NO certification should ever be relied upon as a seal of trust. Trust only begins when Mr. Advisor is representing you in the capacity of a fee-only fiduciary, and really on an hourly, one-time or one-task basis. It should also be noted that the CFP board collects an annual $325 fee from all CFP's. One can't help but ponder conflicts of interest.

Registered Investment Advisors (RIAs) must meet a fiduciary standard, although this certification is meaningless unless they stipulate in writing that they will work for you in the capacity of a fee-only fiduciary.

Never seek personalized investment advice from other fee-based non-fiduciary "advisors" such as insurance agents or bank employees. If you choose to seek help with investing or financial planning then your first line of defense is always to be certain that you are at all times working under written contract with a fee-ONLY fiduciary on a ONE-time consultation or ONE-task basis. This legally eliminates the potential for the most common conflicts of interest.

The non-fiduciary "Suitability Standard" that supposedly protects you by law is nothing short of a joke!

Never lose sight of the fact that non-fiduciaries are nothing more than salesmen. Brokers and other non-fiduciaries love to falsely put you at ease by telling you that the law requires them to only sell investments that are "suitable" for the client. Sounds like you're safe and secure right? Wrong! Unfortunately this "suitability standard" is a joke and will not protect you from being sold more expensive and more inferior financial products! The suitability standard is the problem! Licensed brokers are legally allowed to select investments for their clients based on how much commission money they stand to earn or earn for their company. Accordingly expect your broker to sell you the very investments that you should be AVOIDING -- namely long term, illiquid investments with high fees, front end loads or back end loads, higher taxes, higher risk, etc. For example an actively managed mutual fund with no front-end load may seem like a sound investment until you compare the high fees with equivalent ETF's. If you insist on seeking financial advice from someone, then never let them broker the deal, process the paperwork, etc. That means only work with a fiduciary. After you pay for their advice, then you should process your investment transactions on your own via a deep discount brokerage firm. Discuss this with them up front.

Never lose sight of the fact that non-fiduciaries are nothing more than salesmen. Brokers and other non-fiduciaries love to falsely put you at ease by telling you that the law requires them to only sell investments that are "suitable" for the client. Sounds like you're safe and secure right? Wrong! Unfortunately this "suitability standard" is a joke and will not protect you from being sold more expensive and more inferior financial products! The suitability standard is the problem! Licensed brokers are legally allowed to select investments for their clients based on how much commission money they stand to earn or earn for their company. Accordingly expect your broker to sell you the very investments that you should be AVOIDING -- namely long term, illiquid investments with high fees, front end loads or back end loads, higher taxes, higher risk, etc. For example an actively managed mutual fund with no front-end load may seem like a sound investment until you compare the high fees with equivalent ETF's. If you insist on seeking financial advice from someone, then never let them broker the deal, process the paperwork, etc. That means only work with a fiduciary. After you pay for their advice, then you should process your investment transactions on your own via a deep discount brokerage firm. Discuss this with them up front.

Remember that certifications are not the critical determinate in selecting an advisor (if you need help investing). The most important question is whether your advisor is a fee-ONLY fiduciary or not. They must accept fiduciary duty to you in writing (via a signed contract), and provide you with copies of both parts of a "Form ADV", and a written disclosure of exactly how they will / may be compensated for their services and list any potential conflicts of interest. Also avoid "asset managers". It doesn't do you any good if they are charging you on a percentage basis year after year. You want to hire them typically on an hourly, one-time or one-task basis.

Pop quiz question:

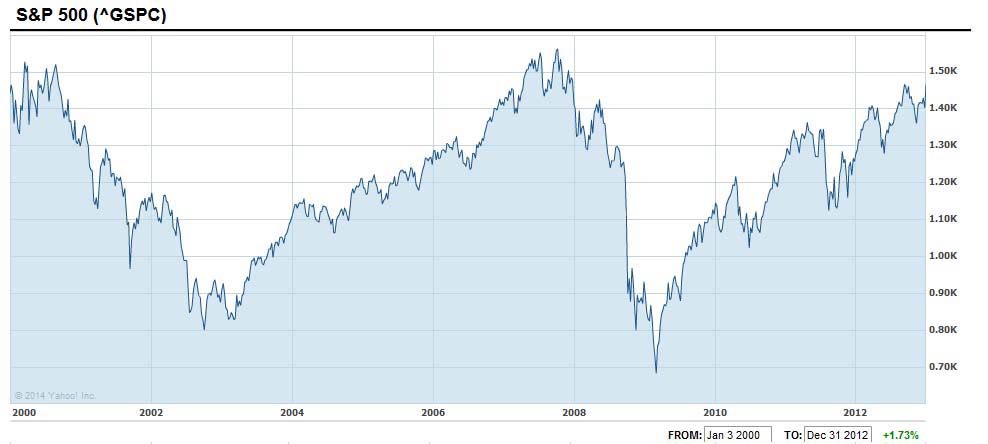

From January 1, 2000 until January 1, 2013 the S&P 500 price return index only gained 1.73%. That's not 1.73% per year but 1.73% for that entire 13 year period! So how much did $100,000 (with 25% invested in an S&P 500 index fund and 75% in 10-year Treasury bonds) grow to by the end of 2012 if dividends and interest were reinvested, and a simple annual rebalancing strategy was implemented once per year to maintain the 75/25 ratio?

{kind=link}

A) $110,316 --- B) $148,084 --- C) $176,459 --- D) $218,904

CLICK HERE for the answer

Tsunami of Sharks

Commission-based "advisors" prey on investors who are ignorant of how bonds protect against stock market volatility

Some folks have given up on the stock market because they lost a lot of money from 2000 to 2009? But it wasn't the stock market's fault. It was their own fault for failing to diversify into bonds, and this wreaked havoc on their savings. CLICK HERE to read about how diversification into bonds has been protecting investors going all the way back to the 1929 stock market crash. Unfortunately there are commission-based advisors out there who use the volatility of 100% stocks as their strawman argument to sell you inferior, expensive and illiquid financial products like annuities and other alternative investments.

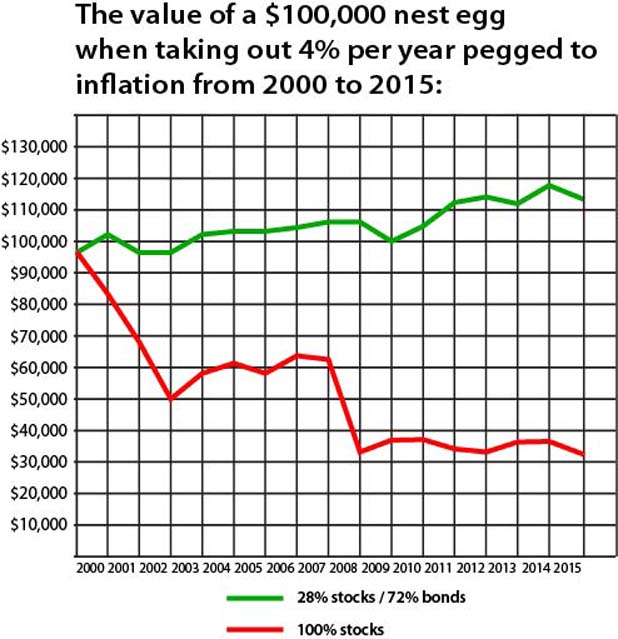

Note: The above chart factors in calendar rebalancing on Jan 1 of every year

Above rate of withdrawal for each year: Jan 2000: $4,000, 2001: $4,136, 2002: $4,251.81, 2003: $4,319.84, 2004: $4,419.19, 2005: $4,538.51, 2006: $4,692.82, 2007: $4,842.99, 2008: $4,978.59, 2009: $5,167.78, 2010: $5,147.11, 2011: $5,229.46, 2012: $5,396.81, 2013: $5,510.14, 2014: $5,592.79, 2015: $5,682.28, 2016: $5,687.96

If you were letting your money just sit and grow, not taking any money out and reinvesting dividents, then from 2000 to the end of 2017 your $100,000 grew to $291,095 for an internal rate of return of 6.11% on an annualized basis. This assumes that you rebalanced your 28/72 mix on Jan 1 of every year. Even with a moderately risky 50/50 mix your 100K grew to $195,727 for a 6.2% annualized internal rate of return.

“If your advisor thinks he can pick winning stocks, choose winning actively managed mutual funds, or time the market -- steer clear!” -- Whitecoat Investor

Many "advisors" prey on investors who are ignorant of what an advisor does

Are you looking for an advisor with a good "track record" who will help you beat the market averages or who will hopefully time the market by anticipating the next market decline and then pull your money to safety? This is not what an advisor should do and this has been confirmed by Vanguard in a memo to investors about the value of an advisor. Therefore avoid any advisor who boasts of having a good track record of picking the best stocks or winning mutual funds, or has been helping his clients beat the indexes. They are selling snake oil. The efficient market hypothesis says that nobody should be able to “beat the market”. Anyone who claims to have been beating the market is either lying or simply taking on more risk, which 1) could backfire at any time, and 2) anyone can do.

If you insist on taking more risk then simply move some of your bond asset class into the stock asset class and / or focus on more volatile indexes (example - a small cap growth index fund like VBK, aggressive growth index fund like AOA). Paying someone to hopefully "beat the market" is a pointless waste of your money. Nobody can predict the next market crash and studies have shown that a strategy that attempts to time the market is more often than not a losing effort that over time doesn't work. Instead an advisor should have you remain constantly diversified while rebalancing from time to time, which anyone can do on their own (without an advisor). Note that rebalancing is not the same as "timing the market".

"Investing is complicated. You need to constantly pay us to manage your money."

Once you have a "game plan" the actual investing and managing of your money is easy. But even fee-only fiduciary advisors have a vested interest in making investing seem complicated so that you will decide to keep paying them year after year. One way to confuse you is to recommend a lot of different funds rather than a simple lazy portfolio of 2 to 5 index funds. There is nothing "wrong" with owning as few as two or three index funds. And any time you can eliminate an annual 1% asset management fee this is a win / win.

Beware of oddball investment products

When non-fiduciary "advisors" try to get their clients to buy annuities, limited partnerships, life settlement investments, whole life insurance, variable life insurance, universal life insurance, pooled funds, house funds, non-traded REITs, and other oddball investment "products" that have "guarantees", "front end loads", "entry fees", "early withdrawal penalties", "early exit fees", "redemption fees" or "surrender fees", they are foaming at the mouth over the giant commission that they will earn. Instead of pitching a mix of stock and bond index funds, they push investments that benefit THEMSELVES or their firm!

When non-fiduciary "advisors" try to get their clients to buy annuities, limited partnerships, life settlement investments, whole life insurance, variable life insurance, universal life insurance, pooled funds, house funds, non-traded REITs, and other oddball investment "products" that have "guarantees", "front end loads", "entry fees", "early withdrawal penalties", "early exit fees", "redemption fees" or "surrender fees", they are foaming at the mouth over the giant commission that they will earn. Instead of pitching a mix of stock and bond index funds, they push investments that benefit THEMSELVES or their firm!

It's usually when investors say "I have given up on the stock market" that they get themselves into trouble through riskier, expensive, under performing alternative investments sold by commission hungry brokers, insurance agents, bank employees and other self-serving salesmen, none of whom legally work for you. You should know that over long time periods of 10 to 15 years it is stocks that have historically been the best performing asset class. The best, most successful and most promising companies and investments are liquid and publicly traded (as stocks or as stock or bond index funds) all sold for less than $10 per trade through any deep discount brokerage. In this day and age there is NO NEED to invest your money in illiquid oddball investments that you can't touch for a number of years. With over 6,500 listings traded on the stock exchanges there is absolutely no reason why an investor would need to look elsewhere.

Regardless of whether you do it yourself or work with an advisor, the only investment checks you write should always be paid to the order of your deep discount brokerage firm (such as E Trade, Scot trade, TD Ameritrade) or light advice company (such as Vanguard)!

Critical line of defense: If an investment is not sold through your deep discount brokerage firm then don't touch it! Never ever ever hand your investment money over to anyone else! This way no advisor can access, control or steal your money. It follows that you should never hand investment money to any investment planning firm or individual, financial consultant, money manager, retirement planner, estate planner, investment strategist, registered representative, advisor, proprietary offering, trust, insurance company, etc.

One exception are "light" advice companies such as Vanguard, Fidelity and Schwab. Vanguard only charges a 0.3% annual management fee.

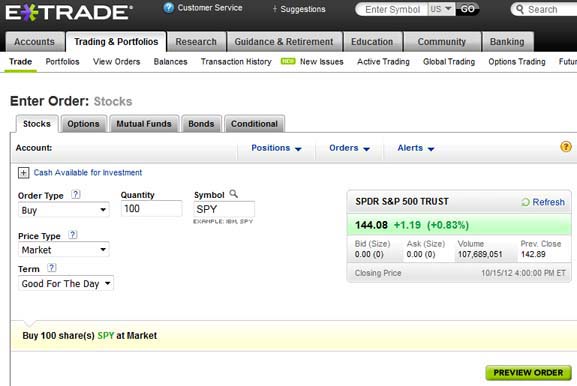

If you can't invest in it by placing an order through your deep discount brokerage then by default you ought to consider it inferior, riskier than disclosed, a scam or a high commission based investment product that a broker, insurance agent or bank employee is trying to sell you. Buying securities online is incredibly simple and easy, and by default you can only buy publicly traded investments. Deep discount brokerage firms only provide trading services while you do all of your decision making and investing yourself. I happen to use E Trade, but others include AmeriTrade and Scot trade. Deep discount brokerages do allow you to purchase mutual funds of all flavors, but after doing your own due diligence, you will want to avoid "actively managed" mutual fund products in favor of "passively managed" funds which merely track indexes (also known as ETF's or index funds). "Passively managed" funds consistently outperform "actively managed" funds and have MUCH lower fees. Also beware that deep discount brokerages also allow you to purchase penny stocks, but after doing your own due diligence and reading this article on Pump & Dump hopefully you will know to avoid those as well. Instead stick with broad market index funds (ETF's).

Placing an order to buy an index fund is very easy through deep discount brokerages like E Trade, AmeriTrade, or Scott Trade. And whether you buy a thousand dollars worth of shares or a hundred thousand, it's still just a $10 trade! Compare that with whatever Mr. Broker is trying to sell you! (WARNING: Be sure not to confuse "deep discount brokerage firms" with "full service brokerage firms" which have non-fiduciary "advisors" who by default should be regarded as nothing more than salesmen).

Don't trust ANYONE not just with, but involved with large amounts of your money!

PONZI SCHEMES and other FRAUDULENT SCEMES

All too often investors let their guard down for various reasons, such as when they do business with a company or person who is a friend or referred by a friend or family, someone with high profile clientele, someone nice, charming, charismatic (or even modest and meek), professional, religious, philanthropist, well credentialed, well certified, long established, top rated by publications like Barron's, is a member of an organization that includes the word "ethics", well dressed, young or old, famous, a radio host, has appeared on TV, is a NY Times best selling author, is articulate, an eloquent speaker, high profile with fancy brochures and a nice website, someone well connected, etc. These attributes are not a definitive seal of approval in determining that they can be trusted! Con artists usually fit some or most of these profiles. They're the people you would least expect to rip you off, give bad advice or dis serve you in any way. Ponzi schemes are not rare. Only the highest profile ones get news coverage. In realty Ponzi schemes are constantly being uncovered, and the typical victim of fraud is often affluent and college educated. Also it is not uncommon for advisors to unwittingly solicit Ponzi schemes to their clients. Even the very best intentioned investment advisors and firms sometimes know nothing about the investments they pitch beyond what they’re told by promoters! What good does that do you? Money does not grow on trees and it shouldn't be treated so loosely, yet we constantly hear new stories about everyday people losing big chunks or all of their life savings to some sort of investment fraud, con-artist, Ponzi scheme, bad investment, etc because they broke the most simple, basic rules of investing, that all began when they started working with a non-fiduciary. Had these people simply avoided putting more than 5% in any one investment or avoided investments that are not publicly traded then these investors wouldn't be in such financial ruin.

All too often investors let their guard down for various reasons, such as when they do business with a company or person who is a friend or referred by a friend or family, someone with high profile clientele, someone nice, charming, charismatic (or even modest and meek), professional, religious, philanthropist, well credentialed, well certified, long established, top rated by publications like Barron's, is a member of an organization that includes the word "ethics", well dressed, young or old, famous, a radio host, has appeared on TV, is a NY Times best selling author, is articulate, an eloquent speaker, high profile with fancy brochures and a nice website, someone well connected, etc. These attributes are not a definitive seal of approval in determining that they can be trusted! Con artists usually fit some or most of these profiles. They're the people you would least expect to rip you off, give bad advice or dis serve you in any way. Ponzi schemes are not rare. Only the highest profile ones get news coverage. In realty Ponzi schemes are constantly being uncovered, and the typical victim of fraud is often affluent and college educated. Also it is not uncommon for advisors to unwittingly solicit Ponzi schemes to their clients. Even the very best intentioned investment advisors and firms sometimes know nothing about the investments they pitch beyond what they’re told by promoters! What good does that do you? Money does not grow on trees and it shouldn't be treated so loosely, yet we constantly hear new stories about everyday people losing big chunks or all of their life savings to some sort of investment fraud, con-artist, Ponzi scheme, bad investment, etc because they broke the most simple, basic rules of investing, that all began when they started working with a non-fiduciary. Had these people simply avoided putting more than 5% in any one investment or avoided investments that are not publicly traded then these investors wouldn't be in such financial ruin.

CONFLICT OF INTEREST

CONFLICT OF INTEREST

EXPENSIVE, RISKIER, UNDERPERFORMING INVESTMENT PRODUCTS THAT PAY MR. BROKER BIG COMMISSIONS: There's more than just Ponzi schemes that you need to look out for. Investors are usually completely unaware that they have been victimized by conflict of interest. Investors are dis served every day and usually it isn't even illegal. Understand that non-fiduciary advisors earn large back door commissions even when they don't directly charge you any fees at all. Simply having their name listed on certain investment statements as your "agent", "rep" or "broker" can entitle them to commissions and "trailer fee" commissions without you ever knowing it. How can you trust any advisor to give advice in your best interest when they earn a hefty 5 to 14% commission when they convince you to buy that annuity, limited partnership, or other inferior, expensive investment that has an early withdrawal penalty, but earn nothing extra when touting index funds? "Actively managed" (professionally managed) mutual funds typically pay Mr Broker a 2 - 3% commission, even though unmanaged index funds consistently outperform the average professionally managed fund. Whenever you hear the words "front end load, "entry fee", "surrender fee", "exit fee", "redemption fee" or "early withdrawal penalty" attached to an investment, that's code for "your broker will earn a big sales commission if he can convince you to invest in it". Yet no investment advisor will ever explain to their client the many negative reasons why the securities they are pushing, such as actively managed mutual funds, annuities, are inferior investments because the commissions that they stand to earn are too irresistible. Typically these investment advisors push long term, non liquid investments on clients even though you should avoid putting your money in "prison". In fact SEC (Securities and Exchange Commission) laws actually allow brokers to select investments for their clients based on how much commission they get to earn for themselves as long as the investment is "suitable" for the investor. The problem is that the requirements for what is "suitable" is very low and hardly protects the public enough.

FROM BAD TO WORSE: CHURNING

Non-fiduciary advisors are always looking for justifications to call you to get you to buy new securities as often as possible because their income is dependent on making transactions. But at some point too much trading becomes illegal, even under the low "suitability standard". Churning occurs when a broker engages in excessive buying and selling of securities in a customer’s account chiefly to generate commissions that benefit the broker. Churning is against the law. What constitutes churning is a complex subject that an attorney should tackle, but one thing that can be said is that long-term investments like annuities and mutual funds are almost always not meant to be surrendered short-term.

The Do-It-Yourself option: Buy, hold and rebalance bond and stock ETF's

BUY EXCHANGE TRADED FUNDS (ETF's): Overshadowing all of the many pitfalls of investing is a little known fact that no non-fiduciary 'advisor' will ever tell you, and that is that the statistical evidence is clear that passively managed index funds (example: the Total Stock Market index) outperform actively  managed mutual funds. As of 2014, Warren Buffet recommends that for long-term results the average investor put 90% of their money in the S & P 500 index and the other 10% in short-term government bonds. If you can't figure out how to do it yourself (it's very easy) or what is the right bond/stock allocation then hire a fee-only fiduciary advisor for a one-time or one-task consultation or use a light advice company such as Vanguard. Don't pay 1% to 2% per year to an "asset manager" to hold your hand and simply rebalance.

managed mutual funds. As of 2014, Warren Buffet recommends that for long-term results the average investor put 90% of their money in the S & P 500 index and the other 10% in short-term government bonds. If you can't figure out how to do it yourself (it's very easy) or what is the right bond/stock allocation then hire a fee-only fiduciary advisor for a one-time or one-task consultation or use a light advice company such as Vanguard. Don't pay 1% to 2% per year to an "asset manager" to hold your hand and simply rebalance.

There are super low cost index funds for whatever your investment strategy may be, from aggressive or conservative. Investing in index funds is as easy as opening an account with a deep discount brokerage firm and then placing a "buy" order for less than $10 per trade. And you can can sell an index fund at any time for less than $10, and without the early withdrawal penalties that are typically associated with annuities, limited partnerships, "actively managed" mutual funds, non-traded REIT's, etc. And index funds are generally taxed at the lower, more reasonable "capital gains" rate -- unlike some other investments such as annuities which are taxed as "ordinary income". With index funds you'll have the peace of mind in knowing that nobody can take advantage of you. Even Jim Cramer (MSNBC's Mad Money), who devotes about 99% of his show to discussions about individual stocks, has recommended index funds to those who don't have the time to study stocks. Because he has a TV show devoted to stock picking, he might be biased. In reality most investors who do study stocks and market trends would probably fare better by investing in index funds than if they were to try to beat the indexes by trading stocks and racking up trading costs. According to John Bogle (of the Vanguard fund group) it is a mathematical certainty that over a lifetime you cannot beat the indexes with active management (example- actively managed mutual funds). Source: PBS John Bogle has also said that over the long-term probably only about 1% of managers do better than the market indexes. Source (Skip to 13:14)

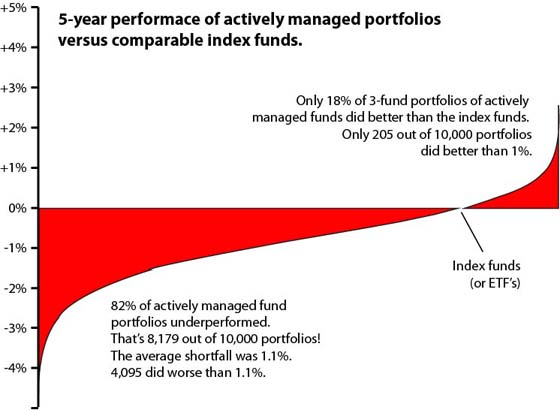

In this 5-year study (ending in June 2012) randomly selected 3-fund portfolios consisting of actively managed funds were compared versus a comparable index fund portfolio. The three funds were intermediate-term municipal bond funds, large cap blend US stocks and large cap blend foreign stocks. A whopping 82% of the actively managed 3-fund portfolios were beaten by the comparable benchmark index fund portfolio. The average "actively managed" portfolio did 1.1% worse than the comparable index fund portfolio. 1.1% might not seem like a lot but when compounded year after year you would lose 10.4% after 10 years. After 20 years it will cost you about 19.8%. And after 30 years 28.2%. In other words small actively manage mutual fund fees matter a lot! See chart below.

"All the time and effort that people devote to picking the right fund, the hot hand, the great manager, have in most cases led to NO advantage.” -- Peter Lynch, legendary manager of the highly successful Fidelity Magellan mutual fund

"By periodically investing in an index fund the know-nothing investor can actually outperform most investment professionals." -- Warren Buffet

"The statistical evidence proving that stock index funds outperform between 80% and 90% of actively managed equity funds is so overwhelming that it takes enormously expensive advertising campaigns to obscure the truth from investors.” -- Peter Lynch

NEXT ARTICLE: Simple basic rules of investing

Disclaimer and Waiver - Nothing on this consumer advocate website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy, hold or sell, or as an endorsement, of any company, security, fund, product or other offering. This website, its owner(s), affiliate(s), agent(s) and / or contributor(s) are not financial or investment advisors or broker / dealers and assume no liability whatsoever by your reliance on the information contained herein. The information should not be relied upon for purposes of transacting securities, assets, financial products or other investments. Your use of the information contained herein is at your own risk. The content is provided 'as is' and without warranties, either expressed or implied. This site does not promise or guarantee any income or particular result from your use of the information contained herein. It is your responsibility to evaluate any information, opinion, advice or other content contained. Always hire and consult with a professional regarding the evaluation of any specific information, opinion, or other content.